Accrual Basis

Accrual Basis :

Ø The income whether received or not but

has been earned or accrued during the period forms part of the total income of

the period.

Ø The firm has taken benefit of a

particular service, but has not paid within that period, the expenses will

relates to the period in which the service has been utilized and not to the

period in which payment for it is made.

Mixed basis : Combination of cash and accrual basis.

System

of Accounting

1.

Single Entry System : This system has no complete record of business

transaction done during a specified period.

2.

Double Entry System : One account is given debit while the

other account is given credit with an equal amount.

Account

: An account is a statement of transactions

affecting any particular asset, liability, expense or income.

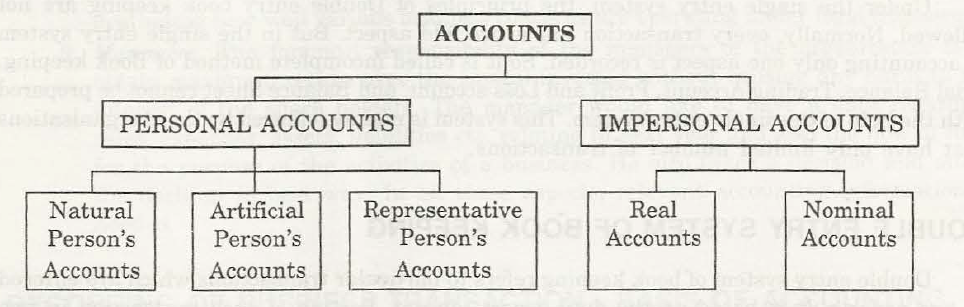

Classification of Accounts :

Nature person’s Personal Accounts: An account recording transactions with an

individual human being is known as a natural person’s personal Accounts. (eg. Krishna Account)

Artificial person’s Personal Account : An account recording financial transaction

with an artificial person created by law or otherwise is called an artificial

person’s personal account. (eg. VSL

College

Representative Person’s Personal Account : An account indirectly representing a person or person is known as a representative account. (eg. Salaries Account)

Representative Person’s Personal Account : An account indirectly representing a person or person is known as a representative account. (eg. Salaries Account)

Tangible Real Account : An assets which can be touched, seen, and

measured. (eg. Machinery Account)

Intangible Real Account : An assets which can’t be touched,

physically but can be measured in value. (eg. Goodwill)

Types

of Accounts

There

are basically three types of Accounts maintained for transactions:

ü Personal Accounts

ü Real Accounts

ü Nominal Accounts

Personal

Accounts

Personal

Accounts are Accounts which relate to persons. Personal Accounts include the

following-

ü Suppliers

ü Customers

ü Lenders

Real

Accounts

Real

Accounts are Accounts relating to properties and assets, which are owned by the

business concern. Real accounts include tangible and intangible accounts. For example-

ü Land

ü Building

ü Goodwill

ü Purchases

ü Cash

Nominal accounts

Nominal Accounts are Accounts which

relate to incomes and expenses and gains and losses of a business concern. For example-

ü Salary Account

ü Dividend

Account

ü Sales

Accounts

can be broadly classified under the following four groups.

ü Assets

ü Liabilities

ü Income

ü Expenses

The

above classification is the basis for generating various financial statements

viz., Balance Sheet, Profit & Loss A/c and other MIS reports. The Assets

and liabilities are taken to Balance sheet and the Income and Expenses accounts

are posted to Profit and Loss Account.

Golden Rules of Accounting

Personal Accounts

|

Real Accounts

|

Nominal Accounts

|

|

Debit

|

The Receiver

|

What Comes in

|

Expenses and Losses

|

Credit

|

The Giver

|

What Goes out

|

Incomes and Gains

|

The

following are the most common source documents.

ü Vouchers

ü Receipt

ü Invoice or

Bill

ü Journals and

Ledgers

ü Cash Memo

ü Debit Note

ü Credit Note

Voucher

A voucher is a document in support of a

business transaction, containing the details of such transaction.

Accounting Vouchers are of two types :

(i) Cash Voucher and

(ii) Non Cash Voucher.

1. Cash Vouchers:

Cash Vouchers

are vouchers that are prepared at the time of receipt or payment of cash. It

also includes receipt and payment through cheque.

Cash Vouchers are of two types:

(i) Credit Vouchers and

(ii) Debit Vouchers.

(i) Credit Vouchers:

Credit Vouchers are vouchers that are prepared at

the time when cash is received.

Cash may be received when:

(i) Goods are sold

(ii) Sale

Format of credit voucher:

Content of Credit Vouchers:

1. Name and address of entity

2. Date of Preparing Voucher

3. Accounting Voucher Number

4. Title of Accounting Credited

5. Net amount of transaction.

6. Narration (a brief description about the

transaction).

7. Signature of the person who has prepared the

voucher.

8. Signature of authorized signatory.

9. Supporting voucher number.

(ii) Debit Vouchers:

Debit Vouchers

are vouchers that are prepared when payment is made. Payment may be on account

of expenses, purchases, drawing of the proprietor, payment to creditor etc.

Format of Debit Voucher:

Accrual Basis

Reviewed by Unknown

on

19:57:00

Rating:

Reviewed by Unknown

on

19:57:00

Rating:

Reviewed by Unknown

on

19:57:00

Rating:

{kind=link}

{kind=link}

{kind=link}

No comments: